College costs keep climbing. For the 2024–25 year, a single year of tuition, fees, housing, and meals now averages about $30,000 at public universities and more than $60,000 at private colleges (BestColleges). Yet 4 in 10 parents haven’t started saving because they “never found time to research the options.” We can change that.

Over the next few minutes, we’ll compare five proven ways to grow education funds and score them on what matters most: tax breaks, financial-aid impact, contribution limits, flexibility, and fees.

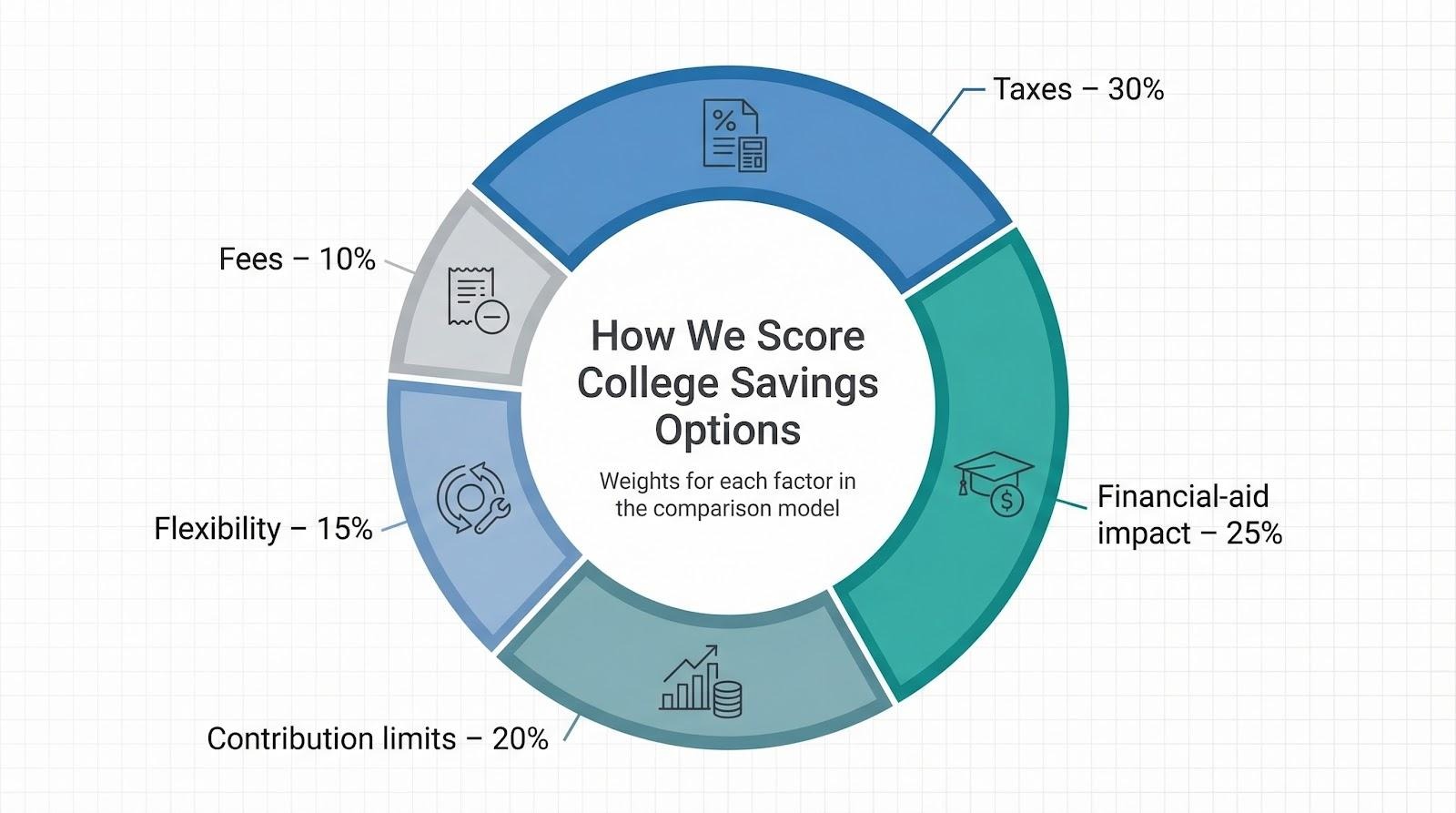

First up: how we built the scoring model—then the heavyweight 529 plan.

Parents need a clear, consistent yardstick, so we built one before looking at the numbers.

We asked what families care about most when choosing a college account. Five priorities rose to the top: meaningful tax savings, minimal impact on financial aid, generous contribution room, flexibility if plans shift, and low, transparent fees.

We turned those priorities into a weighted score so every option faces the same scrutiny. Taxes make up 30 percent of the score, because untaxed growth drives long-term returns. Financial-aid impact counts for 25 percent; contribution limits get 20 percent; flexibility 15 percent; and fees the final 10 percent.

Every vehicle you’re about to read was measured against that rubric. Now, let’s see which one comes out ahead.

Many rely on low-cost index funds, keeping fees modest while the balance compounds.

Illinois’s Bright Start 529 shows what that can look like in practice; its resource Comparing the best ways to save for college maps out how 529s outperform Roth IRAs and bank savings accounts on tax perks, contribution caps, and financial-aid treatment.

Morningstar’s 2024 review gave the plan a Gold rating and reported average expense ratios near 0.05 percent, versus about 0.46 percent for age-based 529 portfolios industry-wide.

Illinois taxpayers can also deduct up to $10,000 of Bright Start contributions each year ($20,000 for married joint filers), layering a state-tax benefit on top of those ultra-low fees.

Investors should consider their own state's tax benefits and fees when choosing a 529 plan.

Think of a 529 as a greenhouse for tuition dollars: you add after-tax money, choose an investment mix, and any growth stays sheltered from federal tax as long as the withdrawal funds education.

Each state offers its own plan, and you can shop nationally. Many rely on low-cost index funds, keeping fees modest while the balance compounds. More than 30 states provide an up-front state-income-tax deduction or credit, giving you a return the day you contribute.

Contribution limits are generous. In 2025, most plans allow lifetime deposits above $400,000 per beneficiary (Utah’s cap is $550,000), so grandparents, aunts, and friends can all add gifts without worrying about a ceiling. Once inside, money can grow for decades, then leave the account tax-free for tuition, fees, housing, or required books.

That mix of high headroom and zero tax on qualified withdrawals is why a 529 often leads every college-savings shortlist. The next issue is how it affects financial aid, which we’ll cover shortly.

Coverdell ESAs rarely make headlines now that 529 plans dominate the conversation, but they still solve a specific need: paying for private K-12 costs and college from one tax-free bucket.

You can open a Coverdell at a bank or brokerage, fund it with after-tax dollars, and invest almost any way you like, from index funds to individual stocks. Earnings grow tax-deferred, and withdrawals avoid federal tax when you spend on qualified education expenses such as tuition, tutoring, books, or a laptop for middle-school coding class.

The catch is the contribution ceiling. As of 2025, each child can receive only $2,000 per year total, no matter how many relatives contribute. In addition, high-income parents phase out of eligibility, which is why many families start with a 529 instead.

Still, a Coverdell pairs well with a 529 when you expect large K-12 bills. Think of it as the flexible spending account of education: the cap is small, the rules are strict, but the tax benefit is meaningful if you drain the balance each year.

One more rule: the student must use the money, or transfer it to a sibling, before turning 30. Miss that deadline, and the IRS will reclaim taxes plus a 10 percent penalty on the earnings.

Bottom line: choose a Coverdell when you want full control over investments and plan to tap funds long before freshman orientation. Otherwise, the higher limits and looser rules of a 529 may serve you better.

Picture a savings account wearing the child’s name tag. That is a custodial account. Adults manage the investments while the child is a minor, but the money legally belongs to the youngster from day one.

Flexibility is the main perk. Funds can cover anything that benefits the child: freshman tuition, a first car, or a gap-year train pass across Europe. There is no college requirement and no withdrawal penalty; you only owe regular taxes on dividends and capital gains.

Taxes can still sting. For 2025, the first $2,600 of a child’s unearned income receives favorable treatment, but earnings above that figure are taxed at the parent’s bracket (IRS Kiddie Tax limits). Over 18 years those yearly bites can slow growth.

Financial aid trims the balance further. The FAFSA treats custodial assets as the student’s money and expects roughly 20 percent of that total to go toward the next academic year, compared with about 5 percent for a parent-owned 529. A $20,000 UTMA could reduce need-based grants by $4,000 a year.

Control also flips at adulthood. When state law says your child is grown—often at 18 or 21—you must hand over the keys. If they spend the fund on crypto or a convertible, that choice is theirs.

So when does a custodial account make sense? Mainly when aid eligibility is not a priority and you want the child to control the money later. Grandparents sometimes use UTMAs as estate gifts. High-income families who expect no need-based aid may also park extra cash here, trusting the future adult to handle it responsibly.

For college-first savers, the math is blunt: taxes drag, aid suffers, and control disappears just when guidance still matters. Keep those factors in mind before placing tuition dollars in a custodial bucket.

Retirement first, college second: that order explains why many planners treat the Roth IRA as a versatile option for family finance.

You add after-tax dollars, invest broadly, and let earnings grow tax-free until retirement. The education loophole adds flexibility. You may withdraw contributions at any time, and you can take out earnings for qualified higher-education costs without the ten-percent early-withdrawal penalty. Ordinary income tax still applies to those earnings, but the bill is often smaller than student-loan interest.

Because the money sits in a retirement wrapper, it does not appear on the FAFSA, which helps preserve aid eligibility during high school. The trade-off surfaces the year after you take a taxable distribution, when that income shows up on the next aid form. One workaround is to use the Roth in junior or senior year, when fewer FAFSAs remain.

Contribution limits remain modest. For 2025 the IRS caps combined Roth and traditional IRA contributions at $6,500 per adult ($7,500 if you are 50 or older), so a Roth alone cannot cover four years at a private college. It shines as a safety valve. Fund your 529 up to any state-tax break, then route extra savings to Roth IRAs. If tuition runs high, the Roth provides a ready reserve; if scholarships cover costs, the money keeps compounding for retirement.

Parents age 59½ or older gain added flexibility. At that point every Roth dollar, contributions and earnings alike, can leave the account tax-free and penalty-free, effectively turning the Roth into a large 529 with broader uses.

Remember, tapping a Roth for tuition reduces retirement funding. Follow the airline-oxygen rule: secure your own financial mask first. Still, for combined flexibility and tax power, the Roth IRA is hard to beat.

Sometimes the simplest option wins. A high-yield savings account or a regular brokerage account in your name offers maximum freedom and zero fine print.

Need the money next semester? Swipe it. If your child takes a gap year or chooses trade school, you can reroute the cash to another goal, such as an emergency fund, a down payment, or even your own sabbatical.

Flexibility carries a cost. Interest, dividends, and capital gains face tax every year, and that drag compounds just like returns, so the final balance may trail what a 529 or Roth IRA can produce over eighteen years.

Financial-aid math lands in the middle. Assets held in a parent account count at about 5 percent under the 2025–26 FAFSA formula—gentler than the 20 percent hit on custodial accounts but still higher than keeping funds inside a retirement plan. Realize large gains right before filing, and the added income can lift your Expected Family Contribution.

Timing matters. Savings accounts work best for short goals—tuition due within one to three years—because principal is safe and today’s top national yields hover near 4 to 5 percent APY. Money earmarked for later years benefits more from the tax shelter of a 529. A blended approach often wins: hold one year of costs in cash for certainty and let the rest grow in a tax-advantaged vehicle.

Bottom line: plain accounts are ideal overflow buckets once you have maxed state 529 deductions and retirement contributions, or when pure liquidity matters most. Just remember, the IRS will claim a small slice each year for that freedom.

No single account tops every category, so the smart move is to stack their strengths.

Start with a 529 up to your state’s tax-deduction limit. That locks in the richest benefit: federal tax-free growth plus an instant state rebate.

Next, send extra savings into a Roth IRA for you (and your spouse, if applicable). You grow retirement security while keeping an emergency valve for tuition gaps.

Then keep about one academic year of expenses in a high-yield savings account or a short-term Treasury ETF. Cash cushions the first tuition bill and prevents selling stocks in a down market.

Review the mix each spring. Adjust contributions, shift 529 investments toward lower risk as graduation approaches, and keep grandparents in the loop so their gifts land in the most aid-friendly spot.

Q1. Will saving in a 529 hurt our financial-aid package?

Not much. Under the 2025–26 FAFSA formula, a parent-owned 529 counts as your asset, and aid calculators expect at most about 5 percent of the balance to go toward next year’s costs. Withdrawals do not count as income. Translation: every $1,000 you save may trim aid by roughly $50 yet still covers the full $1,000 in tuition. That is a worthwhile trade.

Q2. What if my child wins a big scholarship or skips college?

You are not trapped. You can:

Flexibility is built in; no dollar should go to waste.

Q3. Is a Roth IRA safe to tap for tuition?

Yes, if you set limits. You may always retrieve your contributions tax-free, and you can withdraw earnings for qualified education costs without the ten-percent early-withdrawal penalty. You will owe income tax on those earnings, and removing funds can slow retirement growth. Use the Roth as a relief valve, not the primary reservoir, and you can keep both college and retirement goals on track.